The plan is the latest White House effort to deal with one of the most critical impediments to economic recovery—a stagnant housing market caused in part by a surfeit of homeowners who are unable to refinance.

The overhaul will, among other things, let borrowers refinance regardless of how far their homes have fallen in value, eliminating previous limits. That could open up refinancing to legions of borrowers in Nevada, Arizona, Florida, California and elsewhere who are paying high interest rates and are deeply "underwater," owing more than their houses are worth. President Barack Obama is expected to tout the program in Las Vegas on Monday.

[More from WSJ.com: Twelve Questions on Obama's Refi Plan]

The plan will streamline the refinance process by eliminating appraisals and extensive underwriting requirements for most borrowers, as long as homeowners are current on their mortgage payments, according to administration officials and an official at the Federal Housing Finance Agency. Fannie and Freddie have also agreed to waive some fees that made refinancing less attractive for some.

The revamp is aimed at homeowners like Christine and Hector Penunuri of Gilbert, Ariz., who have never missed a mortgage payment and who both have jobs and good credit. Yet their application to refinance their five-bedroom home, which has fallen in value, was denied earlier this year because their tax returns showed a $1,000 loss in start-up costs from Mr. Penunuri's business, which isn't even his day job.

It's "absurd," says their mortgage broker, Steve Walsh of Scottsdale, because the loan is already guaranteed by government-backed mortgage company Freddie Mac.

The Penunuris could save $350 a month by refinancing to a 4% rate from their current 5.75%. They would use that money to put their two sons into junior sports, take a family vacation and pay off other debts, says Ms. Penunuri, 41 years old. "It's a win-win situation."

Freddie Mac declined to comment on the rejection of the Penunuris' earlier refinancing. Freddie Mac and sister company Fannie Mae together guarantee roughly half of the nation's $10.4 trillion in home loans outstanding.

Regulators are revamping a program rolled out two years ago, the Home Affordable Refinance Program, or HARP, which lets borrowers with less than 20% in equity refinance if their loans are backed by Fannie Mae or Freddie Mac. President Obama announced HARP roughly one month into his presidency. So far, only 894,000 borrowers have used it, of which just 70,000 are significantly underwater.

"It hasn't worked," said James Parrott, a White House economic adviser, in a speech last month.

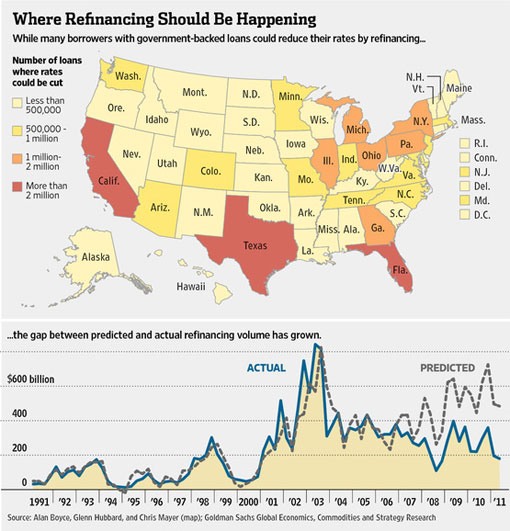

Officials at the Federal Housing Finance Agency, which regulates Fannie and Freddie, estimate that between 800,000 and one million more borrowers should be able to refinance. "It's in our interest to have these borrowers refinance into lower rates and continue to pay," said an FHFA official.

Monday's refinance announcement is separate from a recent push by state attorneys general to extract concessions from banks to refinance underwater mortgages. That effort, part of the months-long negotiations to settle alleged foreclosure-processing abuses, would apply only to loans held on the books of five of the nation's largest banks, a much smaller subset of loans.

In past downturns, lower interest rates engineered by the Federal Reserve were a powerful antidote for a sluggish economy. Falling mortgage rates triggered a refinancing wave that lowered homeowners' mortgage payments, freeing up cash for other things. That, in turn, helped to stimulate spending that boosted economic growth.

This time around, falling mortgage rates—now averaging just 4.11% for a 30-year fixed-rate mortgage, according to a Freddie Mac survey—haven't packed the usual oomph. The reason: Many homeowners haven't been able to refinance.

CoreLogic, a company that tracks 85% of all mortgages, estimates that 20 million borrowers with equity in their homes could cut the interest rates on their loans by more than one percentage point if they could refinance. That's about a quarter of all the homeowners in the country.

Because a refinanced mortgage is treated like a brand new loan, refinancing is nearly impossible for another eight million borrowers whose homes are worth less than their mortgages, unless they qualify for HARP.

But what about those who still have equity in their homes? Some have blemishes on their credit and employment histories or don't have enough income to qualify under today's tougher lending standards. Some find refinancing isn't worthwhile after factoring in new fees imposed by Fannie and Freddie or other closing costs. Still others can't get a refinancing application through a clogged mortgage-processing system.

The changes should help borrowers like Carol Gesior, who has two underwater mortgages, backed by Freddie Mac, on suburban Chicago properties she bought for siblings. She says she tried to refinance but her bank, Citigroup Inc., told her she couldn't without equity. She was unaware of HARP. If she could refinance both properties, she says she would replace her 1995 Ford Crown Victoria.

"I made a commitment. I signed an agreement to pay. But I didn't do anything to cause the values of these homes to decrease," says Ms. Gesior, 52, an office manager at an investment management firm. "Any logical person would have walked away already."

A Citi spokesman says the company is "happy to work with this client to explore refinancing options that may be available to her."

One problem is that bankers or other mortgage originators shy away from refinancing all but the safest borrowers because Fannie and Freddie can force a lender to buy back a loan if underwriting flaws emerge. In response, lenders are asking for extra documentation of incomes and scrutinizing appraisals, steps that raise costs and lead to more denials.

Another obstacle is new fees that Fannie and Freddie charge borrowers with less-than-perfect credit, even if the borrower's existing mortgage is guaranteed by Fannie or Freddie.

The changes being prepared by federal officials should boost refinancing because they will let banks avoid the risk of any "buy-back" on a HARP mortgage as long as borrowers have made their last six mortgage payments and they prove that they have a job or another source of passive income. They are also set to reduce loan fees that Fannie and Freddie charge. The fees will be waived on borrowers that refinance into loans with shorter terms, such as a 15-year mortgage.

Pricing details won't be published until mid-November, and lenders could begin refinancing loans under the retooled program as soon as Dec. 1, according to federal officials. Loans that exceed the current limit of 125% of the property's value won't be able to participate until early next year. The program's expiration date, originally next June, will be extended through 2013. HARP is only open to loans that Fannie and Freddie guaranteed as of June 2009.

Mr. Walsh, the Scottsdale broker, says such changes could lead him to hire "a ton" of new loan officers. "I have a line out the door of people who want to refinance under that program and can't," he says.

Refinancing can't fix the biggest problems eating at the housing market. Tight lending standards and high volumes of foreclosed-property sales are putting pressure on home prices at a time when demand is weak, potentially creating more underwater borrowers.

But refinancing could help those borrowers repair their balance sheets and guard against future defaults. If lenders and regulators successfully execute the changes, they could be "amazingly powerful," said mortgage-market pioneer Lewis Ranieri. "It'll start to create the confidence which is largely what's keeping the system from going forward."

The changes could spur an additional 1.6 million refinanced loans by the end of 2013, assuming interest rates don't rise sharply, according to Mark Zandi, chief economist at Moody's Analytics.

"This is probably my third time in three years," says Mr. Wozniak, a 54-year-old investment adviser who says he has an excellent credit score and lots of equity in both properties.

For others, the hurdles are insurmountable. Appraisals are a big one. When an appraisal shows that a property has too little equity, lenders sometimes order a second appraisal. "You get into these appraisal wars, often at the borrowers' expense," says Marietta Rodriguez, the national director for home-ownership and lending at NeighborWorks America, a nonprofit housing group.

Steven Eisner, a 59-year-old attorney in Haddonfield, N.J., says he expected to sail through the process when he tried to refinance last month because he has good credit and strong income. Instead, he was startled to find that the appraisal on his vacation condo in Bonita Springs, Fla., came in so low he would have needed to ante up $52,000.

He put 25% down when he bought it four years ago. But, because of sagging home prices, his equity has declined to just 10% of the property's value. Refinancing "is simply not worth the trouble," says Mr. Eisner, whose mortgage is guaranteed by Fannie.

Not everyone benefits from encouraging more refinancing, of course. Banks and investors in mortgage-backed securities—including Fannie and Freddie and the Federal Reserve—stand to lose billions if performing loans pay off, leaving investors with cash to reinvest at today's lower rates.

"Somebody's going to get hit. This isn't a free good," says Anthony Sanders, a real-estate finance professor at George Mason University in Fairfax, Va.

That doesn't faze Mr. Eisner. "We've certainly done enough to prop the banks up," he says. "These are loans that everyone knew could prepay."

The success of any refinance push rests not only on whether policy makers can untangle a Gordian knot of technical hurdles, but also on whether they can get buy-in from private-sector players. One major obstacle to refinancing is that the mortgage industry has shrunk. Four big banks now control more than 60% of the mortgage market. Many originators, including the biggest banks, have cut staff or shifted loan underwriters into units working through piles of delinquent mortgages.

New rules designed to prevent independent mortgage brokers—who originate loans on behalf of a bank or other lender—from fleecing consumers have made it harder for them to compete with bigger lenders that aren't subject to the same rules. For example, new compensation rules make it less attractive for brokers to originate smaller or more complicated loans.

The reduced competition has led to longer processing times and higher prices for consumers. When their borrowing costs fall, banks aren't necessarily reducing the rates they charge borrowers by the same amount. Banks with big market share "know they can get away with it," says Thomas Lawler, an independent housing economist in Leesburg, Va. "The market's just not as competitive as it once was."

Industry executives dispute the notion that the market isn't competitive but concede that the industry wasn't ready to handle a surge in applications after rates dropped two months ago.

"Capacity constraints" will be temporary because lenders are hiring more staff, but "in the short run, there's no question that's a challenge," says David Stevens, the chief executive of the Mortgage Bankers Association. Lenders are going "through a lot more checks and balances simply to get a loan approved safely and soundly."

Some spurned borrowers aren't giving up. Barb Skaer, 70, of Appleton, Wis., and her husband wanted to refinance a $402,000 mortgage on a second home that appraised at $547,000 two years ago. She says they have strong credit scores and own part of a manufacturing business that makes bobby pins and hair clips.

Ms. Skaer says their bank, J.P. Morgan Chase & Co., quoted a 4% rate. But she says her loan officer told her she and her husband wouldn't qualify for a new loan because their income from their factory business declined the past two years. A J.P. Morgan spokesman declined to comment.

"Our theory is that if we can afford [the current payment of] $2,189 per month, we should be able to afford $200 less by refinancing," says Ms. Skaer. "This makes absolutely no sense to us, and we are not taking 'no' for an answer."

Nick Timiraos at nick.timiraos@wsj.com

The views, opinions, positions or strategies expressed by the authors and those providing comments or external internet links are theirs alone, and do not necessarily reflect the views, opinions, positions or strategies of First Capital, we make no representations as to accuracy, completeness, current, suitability, or validity of this information and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All registered trademarks, copyright, images, or other items used are property of their respective owner and are used for editorial purposes only.

Visit First Capital Online or call: 310-458-0010

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.